Chargebacks and friendly fraud pose serious challenges for online merchants. Visa’s Compelling Evidence 3.0 (CE3.0) framework, introduced in April 2023, offers merchants a structured approach to combating these issues. This article provides a clear guide to understanding CE3.0, its implications, and practical steps for implementation. Additionally, it highlights the role of partners like Merchanto.org in chargeback prevention.

Understanding Friendly Fraud

Friendly fraud, or first-party fraud, occurs when a customer disputes a legitimate transaction to secure a refund. According to the Mercator Advisory Group, friendly fraud cost merchants globally around $50 billion in 2020. This type of fraud has escalated, especially during the pandemic, driven by economic pressures.

Chargebacks further compound these losses. A single chargeback can cost merchants more than twice the original transaction amount due to fees, lost inventory, and operational costs. Visa reports that 75% of chargebacks are attributed to friendly fraud, highlighting the need for robust solutions like CE3.0.

Overview of Visa Compelling Evidence 3.0

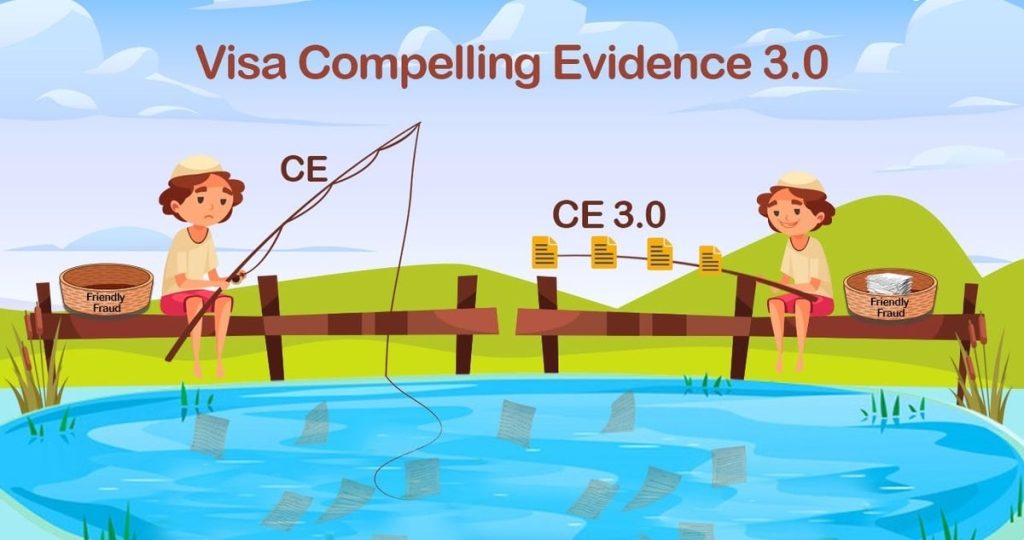

Visa CE3.0 is a global dispute resolution rule designed to reduce chargebacks, particularly those stemming from friendly fraud. It requires merchants to present specific data points as evidence to contest a chargeback, potentially shifting the liability from the merchant to the card issuer.

Key Evidence Requirements

To qualify under CE3.0, merchants must provide at least two of the following data points from previous transactions that occurred 120 to 365 days before the disputed transaction:

- User account log-in ID

- Shipping address

- Device ID or fingerprint

- IP address

This data helps demonstrate the cardholder’s involvement in the transaction, making fraudulent claims more difficult to succeed.

Key Changes in CE3.0

CE3.0 introduces several important changes compared to previous versions:

- Increased Data Requirements: Merchants now need to present at least two matching data points from previous transactions, rather than the single data point required earlier.

- Specific Time Frame: The qualifying transactions must have occurred within 120 to 365 days before the disputed transaction, ensuring that the evidence reflects recent customer behavior.

- Enhanced Security: CE3.0 encourages merchants to adopt stronger security measures, such as integrating technologies like biometrics and encryption, to ensure transactions are secure.

Table 1: Comparison of Visa CE2.0 vs. CE3.0

| Feature | Visa CE2.0 | Visa CE3.0 |

|---|---|---|

| Data Points Required | 1 | 2+ |

| Time Frame | Flexible | 120-365 days |

| Technological Integration | Limited | Includes technologies like biometrics and encryption |

| Applicability | Most transactions | Focus on card-not-present (CNP) transactions |

| Chargeback Liability | Primarily on merchants | Can shift to issuers if criteria met |

Benefits of CE3.0 for Merchants

CE3.0 is designed to help merchants reduce chargebacks and protect revenue:

- Lower Chargeback Rates: By requiring stronger evidence, CE3.0 helps prevent illegitimate chargebacks.

- Revenue Protection: With fewer chargebacks, merchants retain more revenue, which would otherwise be lost to fraud and fees.

- Enhanced Customer Verification: The focus on data points like IP addresses and device fingerprints pushes merchants to implement stronger customer verification processes.

Table 2: Impact of CE3.0 on Merchant Chargeback Ratios

| Merchant Category | Average Chargeback Ratio Before CE3.0 | Expected Chargeback Ratio After CE3.0 |

|---|---|---|

| Digital Goods and Services | 1.5% | 0.8% |

| Physical Goods (High Ticket Items) | 2.2% | 1.2% |

| Subscription Services | 2.0% | 1.1% |

| Overall Average | 1.9% | 1.0% |

Challenges and Considerations

Implementing CE3.0 involves challenges, especially for smaller merchants. To comply, merchants must:

- Invest in Technology: Implement systems that can capture and store the required data points, such as IP addresses and device fingerprints.

- Update Data Storage Policies: Ensure transaction data is stored securely and can be accessed for up to 365 days.

- Integrate with Visa’s Order Insight: This tool helps merchants share transaction data with banks and customers in real-time, preventing disputes from escalating to chargebacks.

Merchants looking to enhance their chargeback prevention strategies should consider working with industry leaders. For instance, Merchanto.org, an official partner of Visa and MasterCard, offers tailored solutions that meet the stringent requirements of CE3.0.

Practical Steps for Implementing CE3.0

To maximize the benefits of Visa CE3.0, merchants should:

- Review IT Infrastructure: Ensure that systems can capture, store, and retrieve the necessary data points.

- Train Staff: Educate your team on the new requirements and prepare them to respond effectively to disputes.

- Implement Strong Customer Verification: Use tools like biometrics and encryption to secure transactions.

- Monitor Chargeback Ratios: Keep a close eye on chargeback ratios to ensure compliance with Visa’s guidelines.

Table 3: Steps to Implement CE3.0 for Different Merchant Categories

| Merchant Category | Key Actions | Tools/Technologies |

|---|---|---|

| Digital Goods | Integrate IP tracking and device fingerprinting | Order Insight, Biometrics, Device ID software |

| Subscription Services | Maintain detailed records of customer interactions | CRM systems, Automated Data Storage Solutions |

| Physical Goods | Enhance shipping and delivery tracking systems | Advanced Shipping Software, Transaction Analysis Tools |

Future Implications

Visa’s CE3.0 is a significant advancement in digital payments. As eCommerce grows, so will the need for effective fraud prevention and dispute resolution mechanisms. CE3.0 not only addresses current challenges but also sets the foundation for future developments in payment security.

Mastercard and other payment processors like Checkout.com and Stripe are likely to adopt similar standards to protect merchants and consumers. This trend toward greater transparency and accountability in digital transactions benefits the entire industry.

Conclusion

Visa Compelling Evidence 3.0 is a powerful tool for reducing chargebacks and protecting revenue. By understanding and implementing the new requirements, merchants can position themselves for success in an increasingly complex digital landscape.

By staying informed and proactive, merchants can navigate the challenges of friendly fraud and strengthen their position in the evolving eCommerce environment.