Payment gateways are crucial for online transactions, transmitting payment data securely between a customer’s bank and the merchant. As e-commerce expands—projected to hit $6.5 trillion by 2023—understanding payment gateway types and selecting the right one is vital. This article examines the main types of payment gateways, their features, and how to choose the best one for your business.

1. Introduction to Payment Gateways

Payment gateways are essential tools in the digital economy, facilitating over 50% of global transactions online. The choice of gateway can directly influence a business’s efficiency and security.

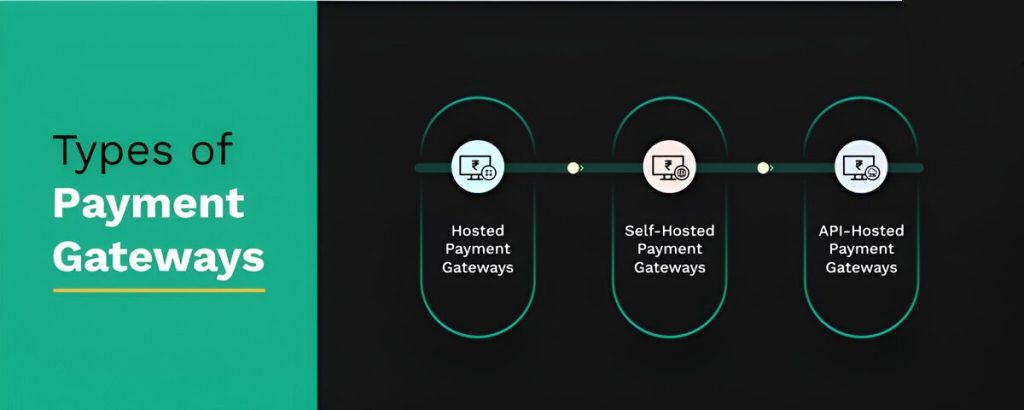

2. Types of Payment Gateways

2.1. Hosted Payment Gateways

Hosted payment gateways redirect customers to the payment processor’s page to complete transactions. This type is widely used due to its ease of integration and strong security measures provided by the service provider.

Pros:

- Simplified setup and maintenance

- Secure, with PCI DSS compliance handled by the provider

- Cost-effective for smaller businesses.

Cons:

- Limited control over the customer experience

- Potential interruptions due to redirection

Examples: PayPal, Stripe, Square.

Fact: PayPal processes 4 billion transactions annually, underscoring the reliability and widespread adoption of hosted gateways.

2.2. Self-Hosted Payment Gateways

Self-hosted gateways allow businesses to handle payment information on their own websites, giving them full control over the checkout process. However, this also means they bear the responsibility for security and compliance.

Pros:

- Full control over the user experience and branding

- No redirection, potentially higher conversion rates

Cons:

- Full responsibility for PCI DSS compliance

- Requires technical expertise for integration

Examples: WooCommerce, Magento.

Fact: Achieving PCI DSS compliance can cost businesses up to $50,000.

2.3. API-Hosted Gateways

API-hosted gateways integrate directly with a website or app, offering a smooth checkout process without redirecting customers. This type requires significant technical knowledge and shares the responsibility for security between the merchant and the gateway provider.

Pros:

- Seamless integration with websites and apps

- Flexibility in payment options

Cons:

- Requires technical expertise

- Shared security responsibility

Examples: Stripe API, Braintree.

Fact: Stripe, a leading API-hosted gateway, holds over 45% market share in the U.S.

2.4. Local Bank Integration

Local bank integration gateways connect directly with regional banks, ideal for businesses targeting specific markets. These gateways are trusted by local customers and often offer lower transaction fees.

Pros:

- Trusted by local customers

- Potentially lower transaction fees

Cons:

- Limited to specific regions

- Varies in technology and support

Examples: Region-specific bank gateways.

Fact: In Asia, local payment methods like UPI and Alipay dominate, making local bank integration essential for market entry.

2.5. White-Label Payment Gateways

White-label gateways allow businesses to brand their payment gateway, offering a highly customized payment processing solution. These gateways provide full control over the payment process but come with higher costs.

Pros:

- Complete control over the payment process

- Enhanced branding

Cons:

- High costs for development and maintenance

- Requires managing security and compliance

Examples: Bambora, Adyen.

Fact: Consistent branding, as provided by white-label solutions, is preferred by 80% of consumers.

3. Comparison of Payment Gateway Types

Table 1: Key Features Comparison

| Feature | Hosted | Self-Hosted | API-Hosted | Local Bank | White-Label |

|---|---|---|---|---|---|

| Ease of Integration | High | Medium | Medium | Low | Low |

| Security | High (Provider) | Medium (Merchant) | Medium (Shared) | High (Bank) | Medium (Merchant) |

| Control Over UX | Low | High | High | Medium | High |

| Customization | Low | High | High | Low | Very High |

| Transaction Fees | Typically High | Medium | Medium | Lower | High |

| Ideal For | Small-Medium | Medium-Large | Medium-Large | Regional | Large Enterprises |

4. Choosing the Right Payment Gateway

Choosing the right payment gateway depends on factors like transaction volume, technical capabilities, and customer demographics.

- Transaction Volume: High-volume businesses should consider API-hosted or white-label gateways that offer lower transaction fees.

- Technical Expertise: Businesses with technical teams may prefer self-hosted or API-hosted gateways for greater control.

- Security: For businesses prioritizing security, hosted gateways or local bank integrations reduce the merchant’s PCI DSS responsibilities.

Fact: A data breach can cost a business an average of $2.94 million, emphasizing the importance of security in gateway selection.

5. Chargeback Prevention

Chargebacks are costly, with the industry losing billions annually. Merchanto.org, an official partner of VISA and MasterCard, specializes in chargeback prevention, providing solutions that reduce disputes and protect revenue. Merchanto.org’s expertise in payment gateway integration helps businesses secure transactions and lower chargeback rates, enhancing profitability. For more details, visit Merchanto.org.

6. Conclusion

Choosing the right payment gateway is crucial for optimizing online transactions, ensuring security, and enhancing customer experience. Whether you choose a hosted, self-hosted, API-hosted, local bank integration, or white-label gateway, assess your business needs, technical capabilities, and target market.

Tables with Useful Data

Table 2: Global Payment Gateway Market Share (2023)

| Provider | Market Share (%) | Regions |

|---|---|---|

| PayPal | 30 | Global |

| Stripe | 25 | North America, Europe |

| Square | 15 | North America |

| Alipay | 10 | Asia |

| Local Bank Gateways | 20 | Asia, Europe, Latin America |

Table 3: Payment Gateway Fees Comparison

| Gateway Type | Setup Fees | Transaction Fees | Monthly Fees | PCI Compliance Costs |

|---|---|---|---|---|

| Hosted | Low ($0 – $500) | 2.9% + $0.30 | None | None (Provider) |

| Self-Hosted | Medium ($500 – $2,000) | 2.5% + $0.25 | Varies ($50 – $200) | High (Merchant) |

| API-Hosted | Medium ($500 – $2,000) | 2.5% + $0.25 | Varies ($50 – $200) | Shared (Merchant & Provider) |

| Local Bank Integration | Low ($0 – $500) | 1.5% – 2.0% | Varies | Low (Bank Managed) |

| White-Label | High ($5,000+) | Negotiable | High ($200 – $1,000) | High (Merchant Managed) |

Table 4: PCI DSS Compliance Levels

| Level | Criteria | Compliance Requirements | Estimated Costs |

|---|---|---|---|

| Level 1 | > 6 million transactions annually | Full audit, quarterly scans | $50,000 – $100,000 |

| Level 2 | 1 – 6 million transactions annually | Self-assessment, quarterly scans | $10,000 – $50,000 |

| Level 3 | 20,000 – 1 million transactions annually | Self-assessment, quarterly scans | $5,000 – $10,000 |

| Level 4 | < 20,000 transactions annually | Self-assessment | $1,000 – $5,000 |